The difficulty curve is not just level-design tuning. In hybrid-casual puzzle games, it is a revenue strategy: the moment a player first feels real friction determines whether spending feels like help, commitment, or punishment.

That is the useful operator lesson from the current sort-puzzle market. PocketGamer.biz’s comparison of Magic Sort, Knit Out, and Pixel Flow frames three games in the same broad genre as three different monetization designs, with nearly $200 million in annual revenue attached to the set.[1] Grand Games’ $70 million Series B adds a funding signal around the same space: short-session hybrid-casual loops are still investable when the operator can show that the loop repeats across titles and teams.[2]

The wrong read is “sort puzzles are hot.” The better read is that the winners are not only choosing themes, ad cadence, or IAP packs. They are choosing when the player should fail for the first time, and what that failure is supposed to do commercially.

Difficulty Is the First Monetization Decision

Most teams talk about difficulty after the core loop is already built. That sequencing is backwards. In a puzzle product, the first serious friction point tells you what business you are actually building.

If friction arrives too early, the game may get quick monetization pressure but weak habit formation. If it arrives too late, the game may build long sessions but under-train players to value boosters, extra moves, or other help mechanics. If friction arrives after the player has already formed a daily routine, spending can feel less like a shakedown and more like protecting progress.

That is why PocketGamer’s most useful claim is not one particular game’s revenue number. It is the argument that the first major difficulty peak can be a stronger predictor of success than early conversion or average-player snapshots.[1] The key question is not “is level 12 too hard?” It is “what commercial behavior should the first hard level create?”

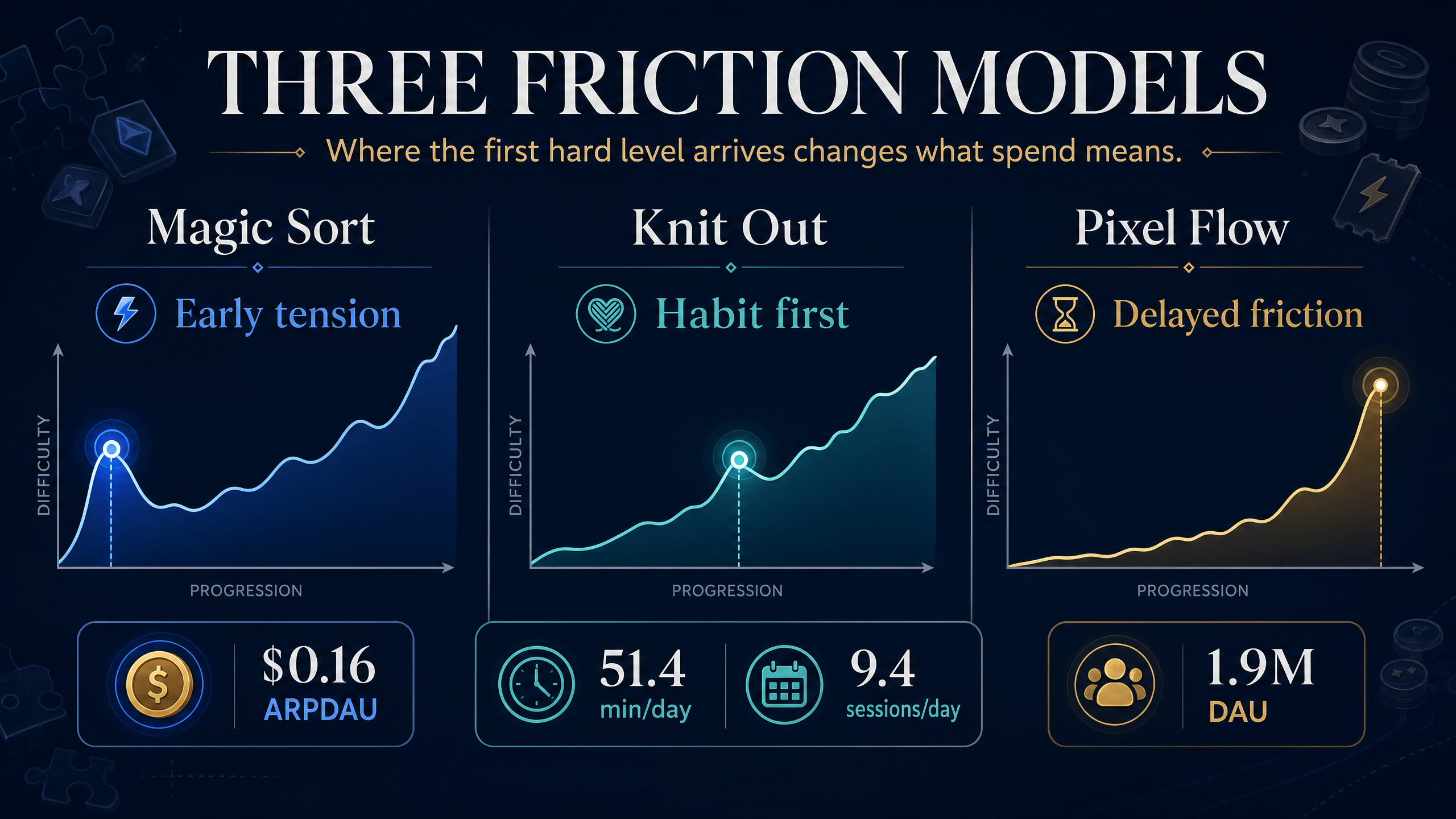

Three Games, Three Friction Models

The useful way to read the sort-puzzle comparison is as a set of operating models.

Magic Sort appears to monetize by creating tension early. PocketGamer cites a relatively high ARPDAU for the genre, but the tradeoff is that early pressure needs careful handling: if the player has not built enough attachment, “help” can feel like a toll booth.[1]

Knit Out is more interesting as a habit-first model. Its pressure is framed as arriving later, after the player understands the loop and has more reason to care about saving progress. That is a different monetization posture: the design is not only increasing difficulty, it is changing the player’s emotional context before asking for relief.

Pixel Flow pushes in the other direction. PocketGamer cites long daily playtime, frequent sessions, and large DAU, which suggests a product that buys scale and routine before applying hard pressure.[1] The risk is obvious: a game can be loved, played, and still leave money on the table if it delays value exchange too far.

None of these approaches is universally correct. The point is that each one implies a different economy. The level curve, ad cadence, booster design, event calendar, and shop strategy have to agree with the same friction model.

Funding Follows Repeatable Pressure

Grand Games’ Series B matters because it gives the category a capital-market signal without turning the article into a funding recap. The company is not being rewarded for one broad genre label. It is being rewarded for an operating claim: it can build short-session hybrid-casual games repeatedly, across titles such as Magic Sort and Block Out.[2]

That is what studios should copy, not the surface theme. A fundable hybrid-casual model has to show that friction can be tuned, tested, and monetized without breaking the daily loop. That requires evidence:

- Failure timing: where the first meaningful loss happens and what it teaches.

- Recovery behavior: whether players retry, watch, spend, or leave.

- Booster meaning: whether paid help preserves mastery or replaces it.

- Event fit: whether events reinforce the core loop or distract from it.

- Channel fit: whether the same promise can survive ads, organic discovery, and store featuring.

This is why “make the game harder” is not a strategy. A good difficulty curve is an economic instrument. A bad one is just churn with a spreadsheet attached.

Web Stores Change the Economy, Not Just the Margin

GameRefinery’s April market review and PocketGamer’s Pixel Federation coverage point to a second piece of the same system: direct purchase paths are becoming part of the operating model.[3][4]

It is tempting to treat web stores as a finance or platform-fee tactic. That undersells the design impact. If more value moves through a web shop, the in-game economy still has to create the reason to buy. Events, currencies, bundles, loyalty rewards, and progression pressure all become part of the route to purchase.

Pixel Federation’s reported Pixel Shop share is a useful reminder: direct-to-consumer revenue does not appear by placing a storefront outside the app.[4] It appears when the game has already trained players to understand value, urgency, and return behavior. The web store captures demand; the product creates it.

What to Audit Before Scaling

A studio does not need to clone the current sort-puzzle leaders. It does need to answer the same operating questions before scaling spend or adding monetization complexity.

1. Where is the first meaningful fail state?

Do not only measure whether players pass early levels. Measure what they learn when they fail, how many retries they tolerate, and whether help feels legitimate.

2. What is the product asking the player to protect?

Progress, streak, collection, event rank, social status, or session flow. If the player is not protecting anything, monetization has to lean on pressure alone.

3. Does paid help preserve mastery?

The healthiest puzzle economies sell relief without making the player feel stupid. If boosters replace mastery instead of preserving it, revenue may spike before retention pays the bill.

4. Do events intensify the right behavior?

Events should focus the core loop, not merely decorate it. A good event gives the player a stronger reason to engage with the same skill, economy, or social loop the base game needs.

5. Is the purchase route aligned with the pressure?

If direct purchase paths, bundles, and loyalty offers sit outside the player’s actual motivation, they will look like margin optimization. They should feel like the natural next step in a loop that already works.

Closing: The Curve Is the Strategy

Hybrid-casual puzzle growth is easy to misread from the outside. The category can look like a set of simple mechanics and quick creative tests. The stronger operators are doing something more precise: they are deciding when players should struggle, why they should come back, and where payment should fit into that emotional sequence.

That makes difficulty design a board-level product question. If the curve is wrong, better ads, richer events, and a cleaner web store will not fix the product. If the curve is right, those systems can compound.

Sources

- PocketGamer.biz, “One genre, three strategies: How Magic Sort, Knit Out, and Pixel Flow are redefining sort-puzzle monetisation” – https://www.pocketgamer.biz/one-genre-three-strategies-how-magic-sort-knit-out-and-pixel-flow-are-redefining-sort-puzzle-monetisation/

- PocketGamer.biz, “Grand Games raises $70m Series B to scale hybrid-casual gaming” – https://www.pocketgamer.biz/grand-games-raises-70m-series-b-to-scale-hybrid-casual-gaming/

- GameRefinery / Liftoff, “Mobile Game Market Review April 2026” – https://www.gamerefinery.com/mobile-game-market-review-april-2026/

- PocketGamer.biz, “Pixel Federation reports $48m revenue in 2025 as TrainStation 3 drives record launch” – https://www.pocketgamer.biz/pixel-federation-reports-48-revenue-in-2025-as-trainstation-3-drives-record-launch/